The Most Expensive Insurance Policy is one That Doesn't Pay!

When people compare life insurance policies, the first number they usually look at is the premium. But do cheap insurance premiums end up costing more? Insurance feels like a cost - until the day you actually need it.

So naturally many people look for the cheapest option. Nothing wrong with wanting value.

But here’s the practical reality: Insurance policies can look similar on the surface while being very different underneath.

Most of the important differences live in the policy wording. And that’s where cheaper policies can sometimes create surprises.

Why Cheap Insurance Looks Appealing

Lower premiums are attractive for obvious reasons. If two policies appear similar and one costs less, the cheaper one looks like the smarter choice. But insurance isn’t quite that simple.

Policies can vary significantly in:

- what situations they cover

- how claims are assessed

- how long benefits are paid

- what conditions are excluded

The Financial Markets Authority (FMA) recommends consumers carefully review policy wording, definitions, and exclusions when comparing insurance products. An independent insurance adviser can help you greatly with comaprisons.

Remember: The premium is only part of the story.

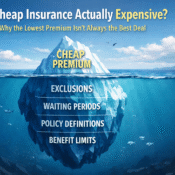

Where Cheap Insurance Policies Often Differ

In plain English, the biggest differences between insurance policies are usually buried in the fine print. Here are some of the areas that can vary the most.

1. Policy Definitions

Insurance claims are triggered by specific definitions written into the policy. Those definitions can be very different between companies.

For example, an income protection policy may define disability in different ways.

Some policies pay if you cannot perform your specific occupation for a specific number of hours a week. Others assess whether you could work in any occupation reasonably suited to your experience or education. Others consider your ability to do the main tasks involved in your occupation. I'm sure that you can see how much of a difference that can have a on whether a claim is approved.

Cancer is cancer, right? But definitions to reach claim criteria can change from one Trauma policy to another.

This is not limited to Income Protection and Trauma Cover. All policy definition differ between insurers. That's why an experienced independent adviser is so important.

2. Exclusions

Every insurance policy contains exclusions. These are circumstances where the insurer will not pay a claim. Some are built in to the policy and others are added during underwriting. If there is no underwriting conducted at application, then it will likely be carried out at claim time.

Common exclusions may include:

- pre-existing medical conditions

- certain mental health conditions

- specific injuries or illnesses

- high-risk activities

Many people only discover exclusions when they try to claim. Despite being clearly outlined in the policy wording. I advise all clients to make sure they check the policy wording for what is covered as much as what isn't. I also ensure that any additional conditions are understood before a policy is accepted.

3. Waiting Periods

Many insurance policies include a waiting period or stand down period before benefits start.

Common examples for income protection include:

- 4 weeks

- 13 weeks

- 26 weeks

- 52 weeks

- 104 weeks

Longer waiting periods reduce premiums but can leave a client vulnerable, with no income. This may mean you need to cover more expenses yourself before payments begin.

Other policies, like Trauma Cover, can have stand down periods for certain conditions like cancer. This can impact new policies and increases to existing policies.

4. Benefit Periods

Another important factor is how long payments last if a claim is approved.

Income protection policies may pay benefits for:

- two years

- five years

- until age 65

- or until age 70

Shorter benefit periods will mean reduced premiums. The reduced premium should be weighed against the loss of long-term protection if someone cannot return to work.

Research from the Financial Services Council NZ highlights how benefit structures significantly affect the financial protection provided by insurance policies.

The Practical Reality

Insurance is one of the few products where the true value often becomes clear only when a claim happens. By then, the policy wording is already locked in and there is no option to correct any mistake.

That’s why the small details matter.

Boring details - but important ones.

What People Often Get Wrong

A common assumption is that insurance policies are mostly the same.

They’re not.

Two policies with similar premiums can operate quite differently when it comes to claims. What is ideal for one person is not an effective solution for another. This is not just clever marketing features to bamboozal clients, this is about ensuring options across the market. Options that will meet specific needs. One size doesn't fit all.

The practical differences are usually in:

- how claims criteria and conditions are defined

- what situations are excluded in the wordign and after underwriting

- how benefits are paid

That’s where the real protection lives.

What To Look At When Comparing Insurance Policies

Instead of focusing only on price, it can help to consider:

- what events actually trigger a claim

- how disability or illness is defined

- what exclusions apply

- how long benefits are paid

- whether the policy structure fits your situation

- what other benefits are included in the policy

There are always trade-offs.

Lower premiums might make sense today but can cause distress at claim time. Especially if the policy doesn't make your exp[ectations. It helps to understand what you're getting, and what you’re not, right from the start.

TLDR:

Cheaper insurance isn’t automatically bad. Expensive insurance isn't always better.

Price alone rarely tells the whole story.

The practical reality is that policy wording matters far more than most people realise.

Benefits have to meet the individual needs and not just their budget.

If You Want a Second Pair of Eyes

If you ever want a second pair of eyes or expert advice before chosing an insurance policy, you're welcome to get in touch. Flick us a message.

Happy to arrange a meeting and talk it through.

No pressure - just a conversation.

Frequently Asked Questions

Is cheaper insurance always worse?

Not necessarily. Lower premiums may reflect different policy structures, waiting periods, or benefit limits. The key is understanding what protection is included and if it meets your needs.

Why do insurance policies have exclusions?

Exclusions help insurers manage risk and keep premiums affordable. However, it’s important to understand what situations are not covered before purchasing a policy. Especially exclusions added after underwriting.

Why do insurance premiums vary between providers?

Premiums vary based on factors such as policy definitions, coverage limits, waiting periods, benefit durations, and the insured person’s age and health.

Thank You for Reading

Thanks for taking the time to read this article and for choosing Cover Yours as a place to learn about insurance and financial protection.

We aim to make complex financial topics easier to understand so you can make informed decisions with confidence.

Disclaimer

This article provides general information only and is not personalised financial advice. You should consider getting advice specific to your situation before making financial decisions. We are happy to help, you can contact us here.

Cover Yours Ltd (FSP769531) and Marc Hamilton (FSP306046) are registered Financial Service Providers and you can search the register here. Marc Hamilton is a member of the FSCL Disputes Resolution Service. Cover Yours Ltd and Marc Hamilton’s disclosures can be found here or by emailing marc@coveryours.co.nz